By 2026, inflation has transitioned from a temporary economic blip to a persistent structural issue that impacts how businesses operate, how they plan their finances, and their choices for the future. Increasing expenses, volatile interest rates, and unpredictable consumer demand are compelling companies to reconsider their established approaches.

For companies operating in dynamic environments, especially in the U.S. market, the key question is no longer “How does inflation impact us?” but rather “How do we adapt and remain stable despite inflation?”

Understanding the Real Impact of Inflation

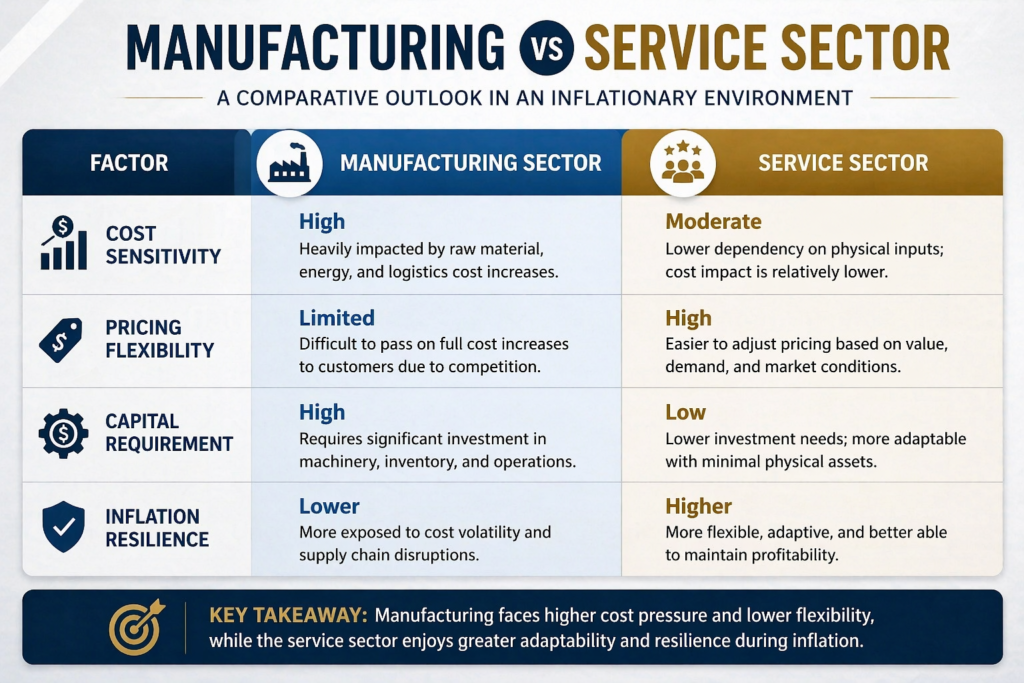

Inflation’s impact on businesses differs, especially between manufacturing and services. It affects production costs, cash flow, and investment. Businesses unaware of these effects face profitability and sustainability issues.

Manufacturing Sector: Direct Exposure to Inflation

Manufacturing businesses are among the most affected during inflationary periods due to their dependency on physical inputs and supply chains.

Key Impact Areas:

- Rising raw material and energy costs directly increase production expenses

- Labor cost pressures due to wage adjustments

- Supply chain disruptions leading to inconsistent pricing

- Reduced profit margins due to inability to fully pass on costs

Unlike other sectors, manufacturing companies face immediate cost pressure, making inflation a critical operational risk.

Working Capital Stress: The Hidden Challenge

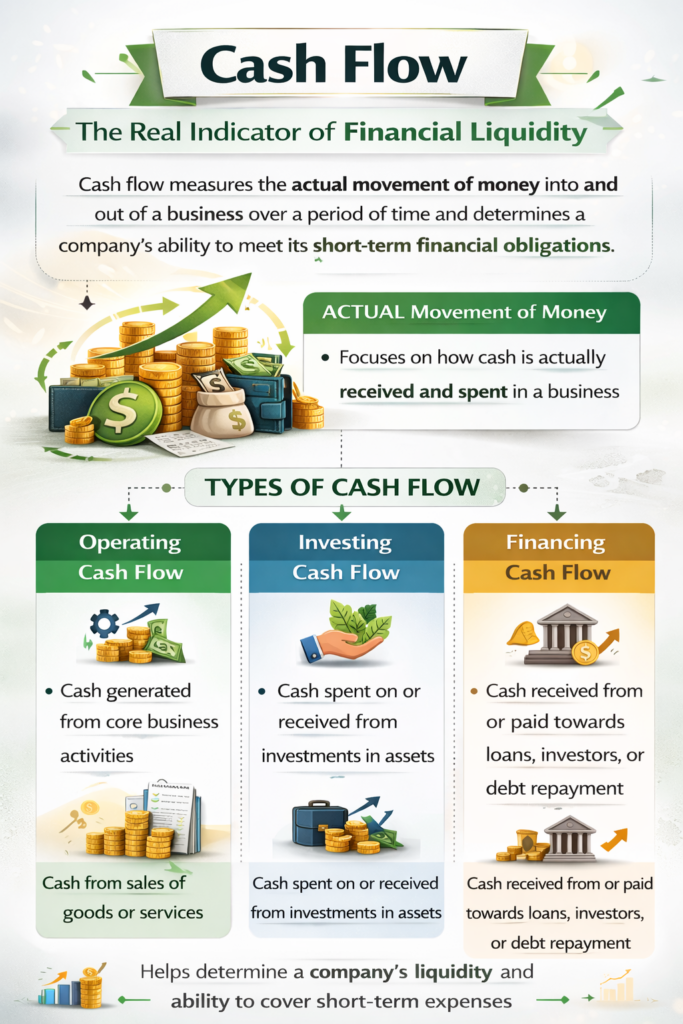

Inflation significantly impacts working capital management, often creating liquidity challenges even when revenues grow.

| Component | Inflation Impact | Business Outcome |

| Inventory | Higher procurement costs | Increased capital blockage |

| Receivables | Slower customer payments | Cash flow strain |

| Payables | Supplier price hikes | Reduced negotiation flexibility |

| Cash Reserves | Lower purchasing power | Liquidity pressure |

Why it matters

A business may appear profitable on paper but still face cash shortages, making working capital management critical during inflation.

Pros and Cons of Inflation: A Balanced Perspective

Advantages (Short-Term Gains)

Inflation can occasionally lead to short-term financial advantages. Companies might see increased income because of higher prices, and goods bought at earlier, lower prices can appreciate in worth. In some instances, reported profits might seem more robust.

Challenges (Long-Term Risks)

However, these benefits are often outweighed by long-term risks. Rising costs compress margins, borrowing becomes expensive, and demand becomes unpredictable. Strategic planning becomes more complex, increasing overall business uncertainty.

Impact on Investment and Expansion Decisions

Inflation and rising interest rates often work together to slow down business growth.

- Cost of borrowing increases

- Capital expenditure becomes expensive

- Expansion plans are delayed or restructured

Strategic Shift

Businesses move from aggressive expansion to cost control and efficiency optimization.

Manufacturing vs Service Sector: Comparative Outlook

Risk Management: A Critical Priority

Inflation introduces multiple financial and operational risks:

- Profitability Risk due to rising costs

- Liquidity Risk due to working capital pressure

- Financing Risk due to high interest rates

- Operational Risk due to supply disruptions

Kariwala Insight

Businesses that actively monitor and manage these risks are better positioned to maintain stability and avoid financial shocks.

How Service Businesses Survive

✔ Adjust pricing dynamically

✔ Shift to remote or hybrid models

✔ Automate repetitive processes

✔ Focus on high-margin services

✔ Reduce dependency on fixed costs

Outcome: Better control over profitability

Strategic Shift: From Growth to Sustainability

In inflationary environments, the focus shifts from aggressive growth to:

- Cost efficiency

- Cash flow stability

- Risk control

Businesses that prioritize sustainability over expansion tend to perform better in uncertain conditions.

Conclusion

In 2026, inflation presents businesses with a strategic shift. Manufacturers face rising costs and reduced profits, while service firms gain from their agility. Success hinges on forward looking financial plans, strict cost control, and robust risk management. Prioritizing long term viability over immediate profits will help companies manage inflation and sustain financial health.

Final Thought (Kariwala Perspective)

Kariwala & Co. LLP posits that during periods of uncertainty, a distinct advantage in the competitive landscape is achieved through financial data clarity and strategic foresight. Enterprises that prioritize organized accounting practices, precise reporting, and proactive analysis are positioned for prosperity, transcending mere survival.