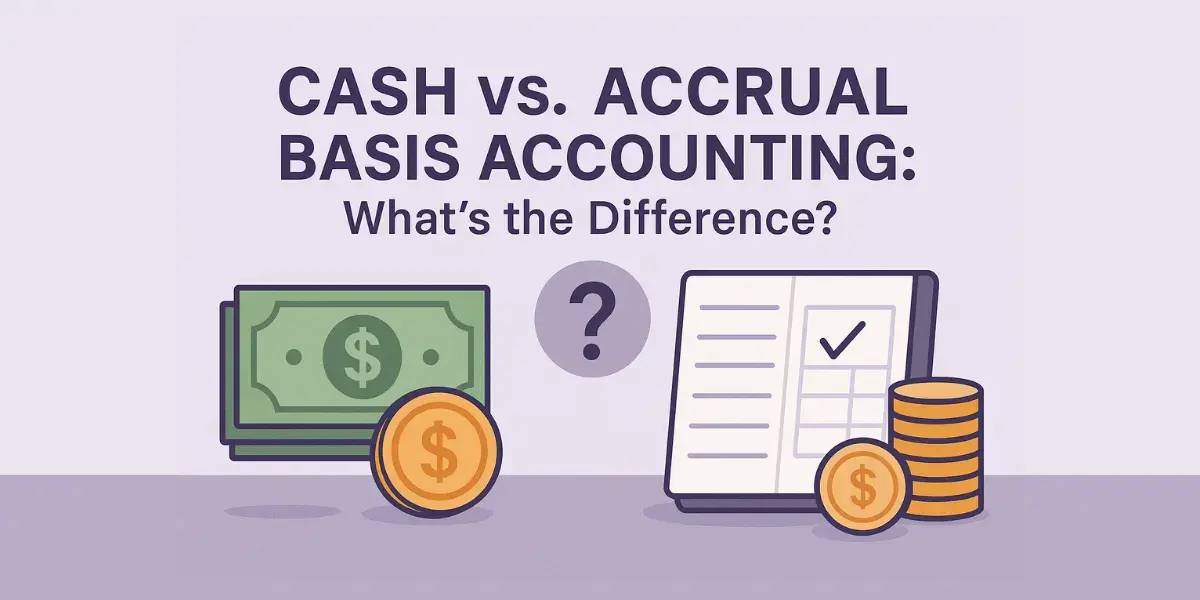

As businesses grow, financial tracking becomes crucial, impacting decisions, compliance, funding, and scalability. Accrual and cash accounting methods influence profitability, tax management, and expansion planning. The right choice at the right time enhances operational clarity and financial control.

The Core Logic Behind the Two Methods

Cash accounting records transactions only when cash actually moves income when received and expenses when paid.

Accrual accounting, on the other hand, records income when it is earned and expenses when they are incurred, regardless of when cash changes hands.

How Each Method Reflects Business Reality

This comparison highlights why many growing businesses eventually transition away from cash accounting as operations become more layered.

What Growing Businesses Prefer and Why

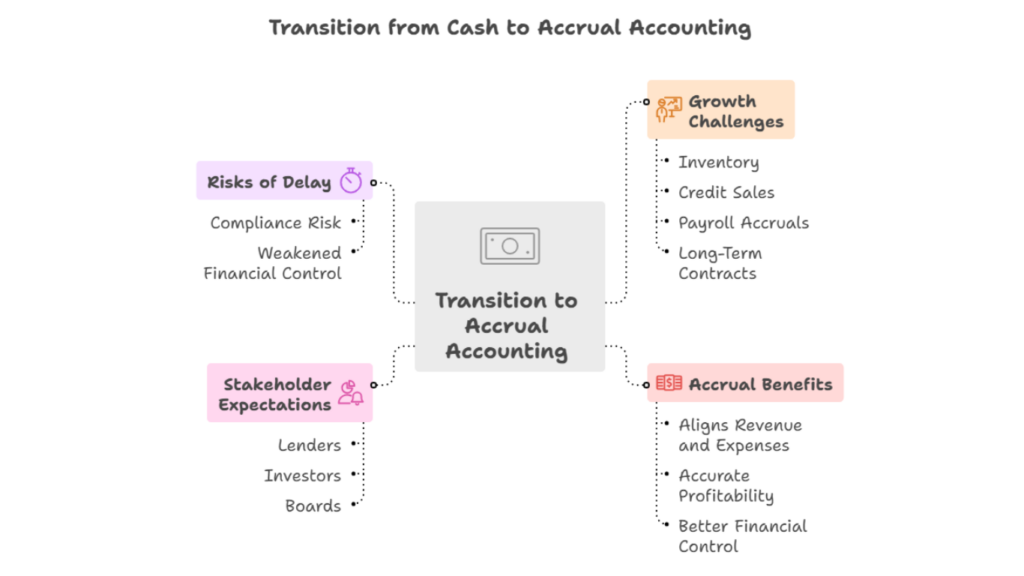

As businesses scale, their preferences tend to shift for practical reasons:

- They need visibility into unpaid invoices and upcoming liabilities

- They require accurate profit measurement, not just cash balance

- They seek easier access to funding and investor confidence

- They must comply with formal reporting standards

For these reasons, accrual accounting becomes the preferred method once operational complexity increases.

Why Early Stage Businesses Lean Toward Cash Accounting

Startups and small businesses often prefer cash accounting because:

- It is easy to understand and implement

- It mirrors bank balance movements

- It requires minimal accounting expertise

At this stage, simplicity often outweighs analytical depth.

Implementation Challenges Businesses Often Underestimate

| Challenge Area | Cash Method Impact | Accrual Method Impact |

| System Setup | Minimal | Requires structured processes |

| Staff Expertise | Basic accounting knowledge | Trained accounting professionals |

| Ongoing Maintenance | Low | Moderate to high |

| Error Risk | Lower complexity | Higher if unmanaged |

Understanding these challenges helps businesses prepare for a smooth transition rather than reacting to compliance pressure later.

Accrual Accounting as a Growth Enabler

Accrual accounting supports expansion by enabling:

- Revenue matching: Income is aligned with related expenses

- Financial forecasting: Future cash flows become visible

- Operational control: Payables and receivables are tracked

- External credibility: Financials align with professional standards

This makes accrual accounting a preferred model for businesses planning long term scalability.

The Compliance and Regulatory

Tax authorities in many places, like the U.S., permit small businesses below certain revenue limits to use the cash method of accounting. However, businesses with inventory, varied income sources, or external reporting needs usually must use accrual accounting. Accrual accounting also produces financial statements that better match GAAP and IFRS, making them suitable for audits, investors, and lenders.

Impact on Performance Interpretation

Under AAP:

- Profit reflects actual business activity

- Management can evaluate trends and margins

- Growth decisions are data-driven

Under cash accounting:

- Profit fluctuates with payment timing

- Performance may appear distorted

Long-term planning becomes difficult

Conclusion

Choosing between cash and accrual accounting affects a business’s finances, growth, and communication. Cash accounting is straightforward and shows immediate cash flow but is less detailed for complex businesses. Accrual accounting, by matching revenues and expenses, better shows profitability, which is vital for growth, funding, or meeting regulations. Growing businesses often need to update their accounting method.

Reference:

FinCEN – Beneficial Ownership Information Reporting (FinCEN.gov)