Why a “Non-Tax” Rule Has Suddenly Become an Accounting Firm Problem

Starting in January 2024, the reporting obligations for Beneficial Ownership Information (BOI) under the U.S. Corporate Transparency Act (CTA) have subtly altered discussions between business proprietors and their financial advisors. What was initially conceived as a measure to combat money laundering and bolster national security has, by chance, become a responsibility for CPA firms, bookkeeping departments, and accounting consultants, frequently without a clear designation of who is accountable.

What Beneficial Ownership Reporting Really Is (And Why Clients Do not get It)

Beneficial Ownership Reporting requires certain U.S. entities to disclose information about individuals who ultimately own or control the company to the Financial Crimes Enforcement Network.

The client confusion stems from three core issues:

- It is not a tax filing

- It does not go to the IRS

- It applies even to small, inactive, or closely held companies

From a client’s perspective, this feels contradictory:

“We’ve already filed with the state, filed taxes, and disclosed owners to banks—why again?”

For accountants, the challenge is translating a legal compliance obligation into language that business owners can understand without providing legal advice.

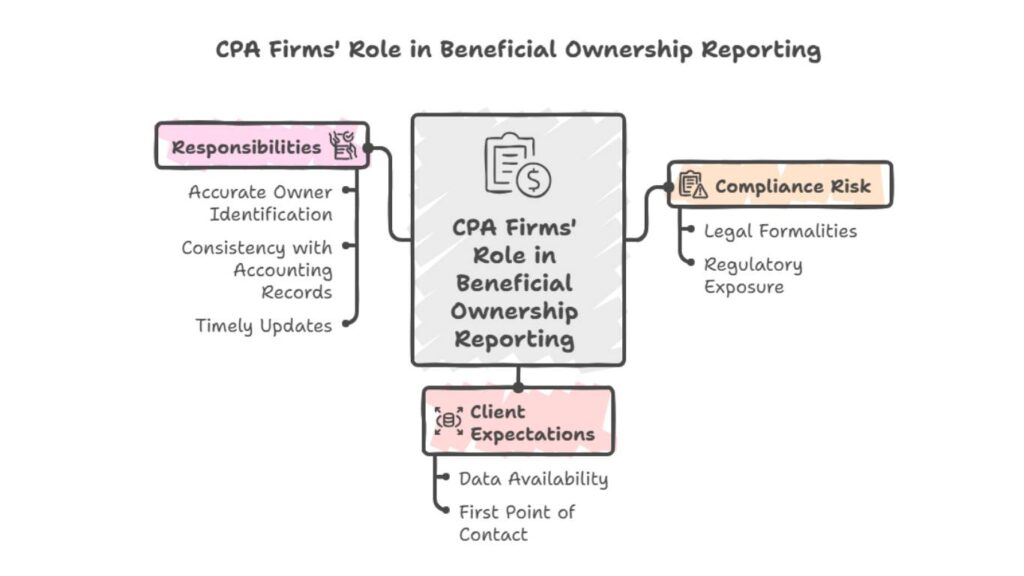

What Accountants Should Track vs. What Lawyers Handle

| Accountants (CPA Firms) | Lawyers / Legal Advisors |

| Collect and maintain beneficial ownership data provided by clients | Interpret legal definitions of substantial control and ownership thresholds |

| Track changes in ownership, officers, and control persons | Advise on complex ownership structures, trusts, and nominee arrangements |

| Assist with compliance timelines and reporting readiness | Determine exemptions, dispute-related ownership, and legal risks |

| Ensure records align with regulatory filing requirements | Handle enforcement issues, penalties, and legal representations |

The Risk Zone for CPA Firms: Where Good Intentions Create Liability

This topic becomes serious because missteps can expose CPA firms to professional risk.

Key risk areas accountants are navigating:

- Interpreting “substantial control” without legal authority

- Advising on ownership thresholds incorrectly

- Filing on behalf of clients without engagement clarity

- Missing updates when ownership changes

- Assuming responsibility by “helping informally”

Many firms are discovering that doing nothing creates client dissatisfaction but doing too much creates liability.

How BOI Reporting Is Affecting Day-to-Day Accounting Engagements

This requirement is already changing how accounting firms operate, even when they are not filing reports themselves.

Practical impacts include:

- Increased onboarding questions for new clients

- Additional entity level documentation requests

- Client emails and calls outside engagement scope

- Time spent explaining rules that are not billable

For firms offering outsourced accounting or compliance support, this adds advisory pressure without defined compensation.

Common Client Misunderstandings (and Why They Ask Accountants)

Why This Topic Matters to CPA Firms

Most U.S. small businesses are encountering this reporting obligation for the first time and are unfamiliar with it. Studies indicate a considerable deficit in knowledge and comprehension, even among businesses mandated to comply, with numerous business owners uncertain if the regulation pertains to them. Consequently, clients are increasingly seeking advice from accountants and CPA firms, despite many of these business owners lacking a grasp of the requirements fundamentals or the data necessary for collection. This situates accountants in a distinctive role as both instructors and dependable consultants.

How CPA Firms Are Adapting Their Service Models

Forward-looking firms are responding strategically rather than reactively.

Some common approaches include:

- Adding BOI discussions to onboarding checklists

- Creating client FAQs or advisory memos

- Offering BOI coordination services (not filing)

- Partnering with legal professionals

- Charging advisory fees for compliance education

- Training staff to recognize red flag structures

This turns confusion into structured advisory value, not free support.

Final Perspective: A Compliance Rule That Redefined the Accountant’s Role

Beneficial Ownership Reporting highlights a broader shift in the profession:

Clients no longer see accountants as record keepers, they see them as compliance guides.

CPA firms that:

- Set clear boundaries

- Educate without overcommitting

- Structure advisory support thoughtfully

- Leverage internal and outsourced teams effectively

will turn this regulatory burden into trusted advisory positioning rather than professional risk.

Conclusion:

Modern CPA firms need robust documentation, clear client communication, and scalable compliance. Increasing regulations and complex client queries demand more than informal methods. Strong accounting operations ensure accuracy, timeliness, and regulatory trust. Structured support and disciplined delivery models enable CPA firms to prioritize advisory and client relationships while ensuring compliance, operational stability, and growth.

Reference:

Beneficial Ownership Information Reporting Rule Fact Sheet (FinCEN.gov)