Bank statements furnish immediate perceptions into a company’s fiscal condition, operational effectiveness, and overall stability. In contrast to conventional financial reports, which offer retrospective summaries, bank records meticulously document the actual movement of capital as it transpires. Vigilant examination of these transactions enables enterprises to leverage favorable developments and proactively identify potential hazards. Ultimately, sustained equilibrium in account balances is indicative of judicious managerial oversight, whereas erratic cash flow patterns suggest underlying operational deficiencies requiring immediate remediation.

Why Your Bank Statement Matters

Cash is a business’s lifeblood, meaning even profitable companies can fail without enough liquidity to cover daily expenses. Bank statements solve this by offering a transparent view of cash movement, serving as a primary tool for tracking financial health.Regular analysis helps businesses optimize budgets, evaluate customer and supplier payment habits, spot anomalies, and make data driven choices. Furthermore, these records allow lenders and investors to verify financial stability when vetting funding requests.

What Your Bank Statement Reveals

| Bank Statement Indicator | What It Indicates | Business Impact |

| Consistent cash deposits. | Stable sales and timely customer payments. | Demonstrates healthy business operations. |

| Increasing bank balance. | Positive cash flow and strong liquidity. | Supports future growth and investment. |

| Declining bank balance. | Cash reserves are reducing. | May create liquidity challenges. |

| Regular supplier payments. | Good financial discipline. | Strengthens supplier relationships. |

| Delayed customer receipts. | Customers are taking longer to pay. | Increases pressure on working capital. |

| Large unexpected withdrawals. | High expenses or unusual transactions. | Requires immediate review. |

| Frequent bank charges | Inefficient cash management. | Reduces overall profitability. |

| Loan repayments. | Existing debt obligations. | Helps assess debt servicing capacity. |

| Seasonal cash movements. | Business is influenced by seasonal demand. | Assists in planning inventory and cash requirements. |

| Growing monthly deposits. | Expanding business activity. | Indicates increasing revenue potential. |

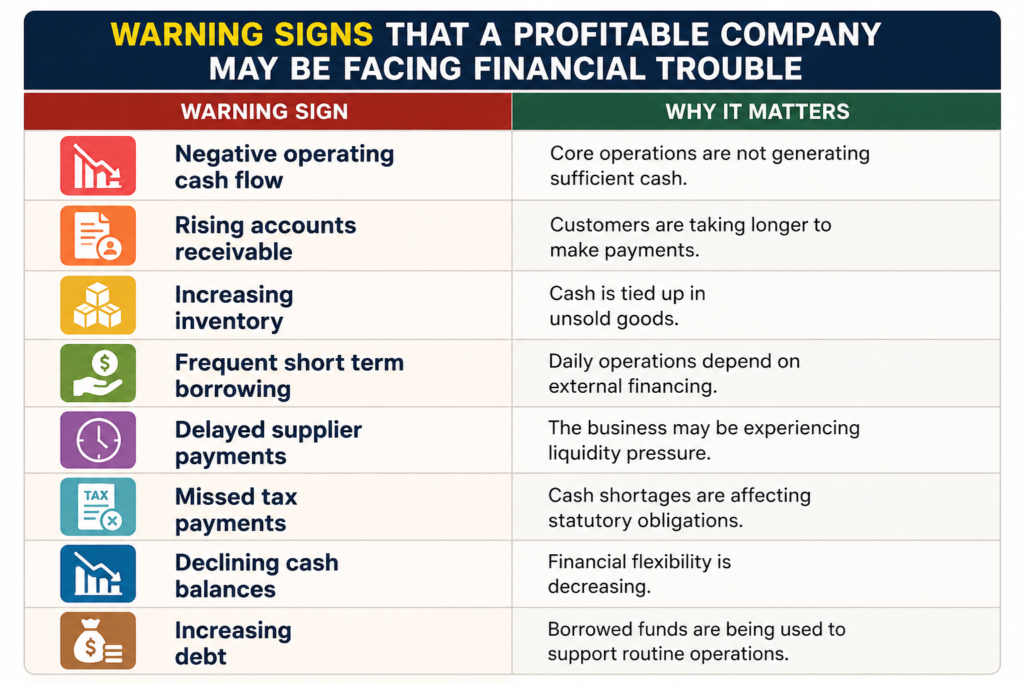

Identifying Financial Risks Before They Escalate

A bank statement can serve as an early warning system for potential financial challenges. Patterns such as declining account balances, delayed customer payments, increasing bank charges, or unusually high withdrawals may indicate underlying issues that require attention. By reviewing these trends on a regular basis, businesses can detect risks before they develop into significant financial problems. Early identification allows management to improve cash flow, strengthen internal controls, reduce unnecessary expenses, and make proactive decisions that protect the company’s long term financial health.

Warning Signs That Require Attention

Certain bank statement patterns reveal hidden financial risks.

- Shrinking Balances: Expenses are outstripping income.

- Lagging Collections: Late customer payments starve operations.

- Frequent Overdrafts: Poor cash planning or debt reliance.

- Mystery Withdrawals: Potential fraud, errors, or double payments.

- Spiking Bank Fees: Inefficient practices or failed transactions.

Spotting these indicators early allows businesses to protect profitability and survival.

Best Practices for Reviewing Bank Statements:

How Regular Statement Reviews Support Business Growth

Regularly reviewing your bank statement helps businesses make informed financial decisions and stay prepared for future challenges. It provides a clear understanding of cash flow patterns, spending habits, and payment trends, allowing management to identify opportunities for improvement and address potential issues early. Consistent monitoring also supports better budgeting, strengthens financial discipline, and ensures the business has sufficient liquidity to support daily operations and long term growth.

The Importance of Maintaining Healthy Cash Flow

Healthy cash flow acts as the primary foundation for business stability and long-term success. While generating profit matters, a company cannot survive without sufficient liquidity to cover daily obligations. Regular bank statement analysis delivers a real-time tracking mechanism, helping management verify that immediate cash can cover payroll, rent, utilities, vendor bills, and debt obligations.

Operational and Strategic Benefits

- Early Problem Detection: Statement reviews quickly flag delayed customer receivables or ballooning operational costs.

- Proactive Interventions: Spotting liquidity trends allows businesses to adjust vendor payment timelines, control expenses, or accelerate collection efforts.

- Financing Growth: Maintaining strong cash reserves allows companies to fund expansions, purchase assets, or absorb unexpected costs without costly debt financing.

Conclusion

Financial statements serve as vital strategic instruments rather than mere administrative documentation. They provide insights into a company’s proficiency in cash management, cost containment, revenue generation, and strategic expansion planning. Periodic examination facilitates the mitigation of risks, enhancement of operational efficacy, and the adoption of forward thinking decision making processes. In essence, continuous oversight identifies emerging prospects and potential impediments at an early stage, thereby fostering a more robust enterprise.