Scenario Overview

In December 2025, a business obtained a loan of ₹10,00,000 at 10% annual interest. In January 2026, the business made a combined payment of ₹1,20,000, which included:

- ₹10,000 for current interest (expense of FY 2025-26)

- ₹10,000 for advance interest (benefit of next financial year)

- ₹1,00,000 towards principal repayment (reduction of liability)

This single transaction affects three different accounting elements:

- Expense recognition (Interest Expense)

- Asset creation (Prepaid Interest)

- Liability reduction (Loan Principal)

Proper classification ensures that profit, assets, and liabilities are presented accurately in the financial statements.

Why Proper Accounting Treatment is Important

If the full ₹20,000 interest is treated as expense immediately:

- Profit will be understated

- Assets will be understated

- Financial statements will not reflect future benefits

Correct accounting ensures:

- Only current period interest is treated as expense

- Advance interest is recorded as a current asset

- Loan balance reflects actual outstanding liability

- Financial statements present a true and fair view

This treatment follows the Accrual Concept and Matching Principle, where expenses are recorded in the period to which they relate.

Complete Accounting Treatment and Financial Position as on 31 March 2026

| Component | Amount (₹) | Accounting Treatment | Effect on Financial Statements | Explanation |

| Loan Taken (Dec 2025) | 10,00,000 | Loan A/c credited | Liability increases | Creates legal repayment obligation |

| Principal Repaid (Jan 2026) | 1,00,000 | Loan A/c debited | Loan reduces to ₹9,00,000 | Improves financial position |

| Interest Paid (Current period) | 10,000 | Interest Expense debited | Expense recorded in P&L | Reduces profit of FY 2025-26 |

| Interest Paid in Advance | 10,000 | Prepaid Interest debited | Recorded as Current Asset | Future benefit available |

| Total Bank Payment | 1,20,000 | Bank credited | Bank balance decreases | Cash outflow occurred |

Closing Financial Position as on 31 March 2026

| Financial Element | Amount (₹) | Financial Statement | Position |

| Loan Outstanding | 9,00,000 | Balance Sheet | Liability |

| Prepaid Interest | 10,000 | Balance Sheet | Current Asset |

| Interest Expense | 10,000 | Profit & Loss Account | Expense |

| Bank Balance | Reduced by ₹1,20,000 | Balance Sheet | Asset reduced |

Key Interpretation as on 31 March 2026

As of the financial year-end, the business has correctly recognized only ₹10,000 as interest expense because it relates to the current accounting period. The advance interest of ₹10,000 remains classified as a prepaid asset, representing future economic benefit.

The loan balance has been reduced from ₹10,00,000 to ₹9,00,000 due to principal repayment. This improves the company’s financial stability by lowering its outstanding obligations.

This treatment ensures that profit is not understated, assets are correctly presented, and liabilities reflect the true financial obligation.

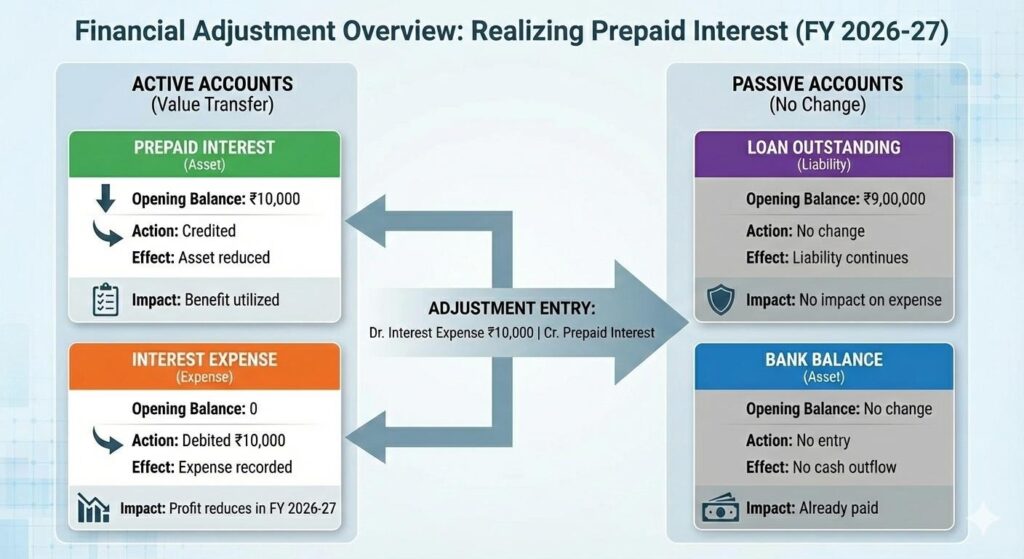

Result in April 2026

In April 2026, the prepaid interest is converted into interest expense because the benefit now relates to the current accounting period. This adjustment ensures proper matching of expense with the relevant period.

No additional cash payment occurs because the interest was already paid earlier. This ensures proper expense recognition without affecting cash flow again.

Overall Accounting Impact Summary

| Component | Treatment | Financial Effect |

| Current Interest | Expense | Reduces current year profit |

| Advance Interest | Current Asset | Future benefit |

| Principal Repayment | Liability Reduction | Improves financial strength |

| Bank Payment | Cash Outflow | Reduces bank balance |

Final Financial Position Interpretation

As of March 31, 2026, the financial statements reflect the correct position of the business. The loan liability stands at ₹9,00,000, prepaid interest of ₹10,000 is recorded as an asset, and only ₹10,000 is recorded as expense in the Profit & Loss Account.

This ensures that profit, assets, and liabilities are accurately reported and financial statements present a true and fair view.

Additional Professional Subtopics

Impact on Profitability and Financial Performance

Proper treatment ensures that only the relevant interest expense is recorded in the current financial year. If advance interest is incorrectly recorded as expense, profit will appear lower than actual, which can mislead management and stakeholders. Correct classification helps in accurate performance evaluation and decision making.

Impact on Balance Sheet Accuracy and Financial Position

Recording advance interest as a prepaid asset ensures that assets reflect future economic benefits. Similarly, principal repayment reduces liabilities, improving the company’s debt position. This ensures the Balance Sheet presents the true financial strength of the business.

Importance for Audit, Compliance, and Financial Transparency

Auditors verify whether expenses, assets, and liabilities are correctly classified. Proper accounting treatment ensures compliance with accounting standards and prevents financial misstatement. This improves transparency, builds investor confidence, and ensures reliable financial reporting.

Conclusion

When a business pays interest in advance along with principal repayment, each component must be accounted for separately. Current interest is treated as expense, advance interest is recorded as a prepaid asset, and principal repayment reduces loan liability. This ensures proper expense recognition, accurate financial reporting, and correct presentation of financial position. Such treatment supports reliable decision-making, ensures compliance with accounting principles, and maintains the integrity of financial statements.

Reference:

IFRS framework issued by the International Accounting Standards Board (IASB)