The Profit Illusion in Modern Businesses

Profitability does not always mean financial stability. While profits suggest a healthy company, many profitable businesses face cash shortages or even bankruptcy. This is because profit measures accounting performance, whereas cash flow indicates the actual money available for operations. This difference is crucial for business leaders, as a company can appear profitable yet struggle with payments.

Understanding Profit in Accounting

Profit is the business’s financial outcome that comes after subtracting expenses from revenue, calculated by accounting rules. Under Accrual accounting, revenue is recorded when earned and expenses when incurred, irrespective of cash transactions.

| Component | Explanation |

| Revenue | Income generated from sales of goods or services |

| Cost of Goods Sold | Direct costs associated with production |

| Gross Profit | Revenue minus cost of goods sold |

| Operating Expenses | Administrative, marketing, and operational costs |

| Net Profit | Final profit after deducting all expenses and taxes |

Because of this accounting approach, profit often reflects economic performance rather than cash position.

The Hidden Gap Between Profit and Cash Availability

Reported profit and available cash can differ due to accounting and operational elements. Revenue recorded before payment boosts profit but not cash. Expenses like depreciation reduce profit without cash outflow, while loan principal payments decrease cash but aren’t expensed. These timing mismatches can lead profitable companies to experience cash shortages.

Real Business Scenario: Profit Without Cash

Suppose, a manufacturing company that sells goods worth ₹10,00,000 in January.

The company records the revenue immediately in its income statement because the goods have been delivered. However, customers are allowed a 90-day credit period, meaning the cash will only be received in April.

Meanwhile, the company must pay for:

- employee salaries

- supplier invoices

- rent and utilities

- loan installments

Although the income statement shows a profit, the business may struggle to meet these payments because the actual cash has not yet been collected.

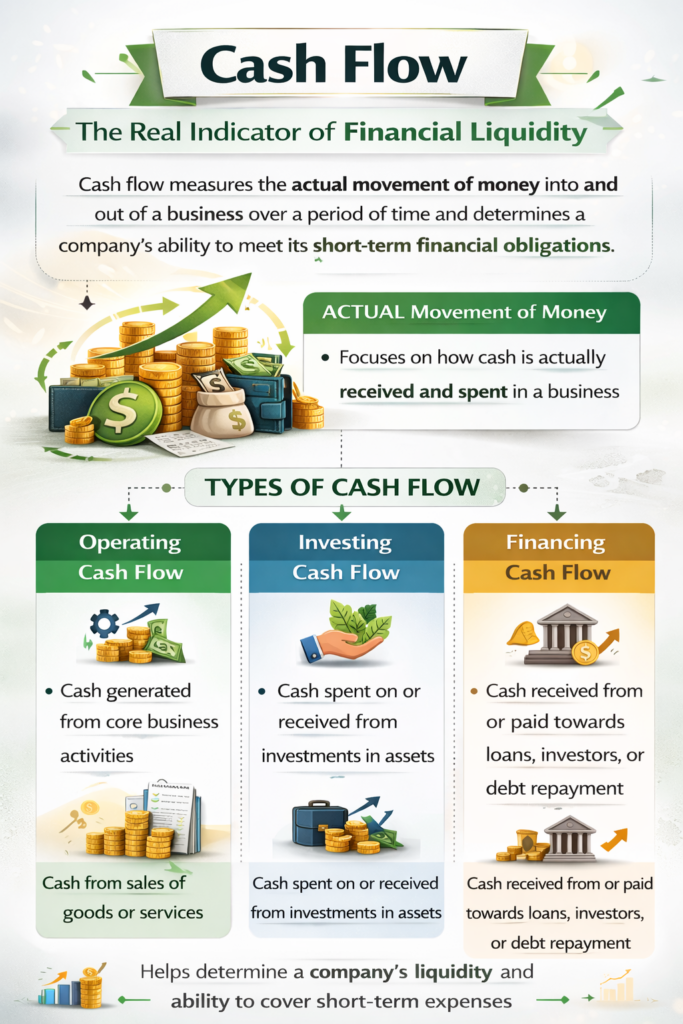

Profit vs Cash Flow: A Practical Comparison

The difference between profit and cash flow becomes clearer when comparing their financial meaning and reporting structure.

| Basis of Comparison | Profit | Cash Flow |

| Financial Statement | Income Statement | Cash Flow Statement |

| Accounting Method | Accrual Accounting | Cash Based Movement |

| Recognition | Revenue and expenses recorded when incurred | Cash recorded when received or paid |

| Purpose | Measures business performance | Measures liquidity and financial stability |

| Impact on Survival | Indicates profitability | Determines ability to operate daily |

This distinction explains why profitability does not always translate into available cash.

Major Reasons Profitable Businesses Experience Cash Shortages

The following operational factors commonly lead to liquidity problems even when profits

are strong.

| Business Factor | Impact on Cash Flow |

| Slow customer payments | Cash remains stuck in receivables |

| Excess inventory | Money tied up in unsold stock |

| Capital expenditure | Large cash payments for equipment or assets |

| Loan principal repayments | Expenses is not reflected as cash outflows |

| Rapid business growth | Increased need for working capital |

Financial Statements and Their Role in Liquidity Analysis

Understanding the relationship between financial statements helps explain how profit and cash flow differ.

The income statement shows profitability during a period.

The balance sheet reflects assets, liabilities, and equity at a specific point in time.

The cash flow statement tracks the actual movement of cash between these periods.

Early Warning Indicators of Cash Flow Problems

Financial analysts often rely on specific ratios and indicators to detect potential liquidity issues before they become critical.

| Indicator | Purpose |

| Operating Cash Flow | Measures cash generated from core operations |

| Current Ratio | Evaluates short term financial strength |

| Quick Ratio | Measures ability to meet obligations without inventory |

| Cash Conversion Cycle | Shows how quickly sales convert into cash |

Practical Strategies to Improve Cash Flow Management

Companies can strengthen their financial stability by implementing structured cash management practices.

Effective strategies include improving receivable collection systems, negotiating better credit terms with suppliers, maintaining optimal inventory levels, and preparing accurate cash flow forecasts.

Businesses should also maintain a liquidity buffer to handle unexpected financial obligations.

Working Capital: The Core Driver of Cash Flow

Working capital represents the funds required to operate daily business activities. It directly influences how quickly a company converts sales into cash.

Working capital consists of three primary elements:

| Component | Role in Cash Flow |

| Accounts Receivable | Money customers still owe to the business for credit sales. |

| Inventory | A business keeps goods in stock to sell or use in production. |

| Accounts Payable | Money the business still owes to suppliers for credit purchases. |

Efficient management of these components helps businesses maintain healthy liquidity.

Conclusion

Profit shows operational success, but cash flow dictates survival and effective operation. A company can seem profitable yet struggle with immediate payments if cash is scarce. Therefore, businesses need to assess both profitability and liquidity. Recognizing the distinction between profit and cash flow, and managing working capital efficiently, ensures lasting financial health and growth.

Reference

https://www.kariwala.pro/services/accounting/