Numerical metrics known as Non-GAAP financial measures are used to modify GAAP results by adding or removing specific factors, such as restructuring charges, stock-based compensation, acquisition-related expenditures, or FX impacts. They can be found in:

- Earnings releases and investor presentations

- MD&A and analyst decks

- Debt covenant reporting and management scorecards

Why Growing Scrutiny-The Regulatory & Market Context

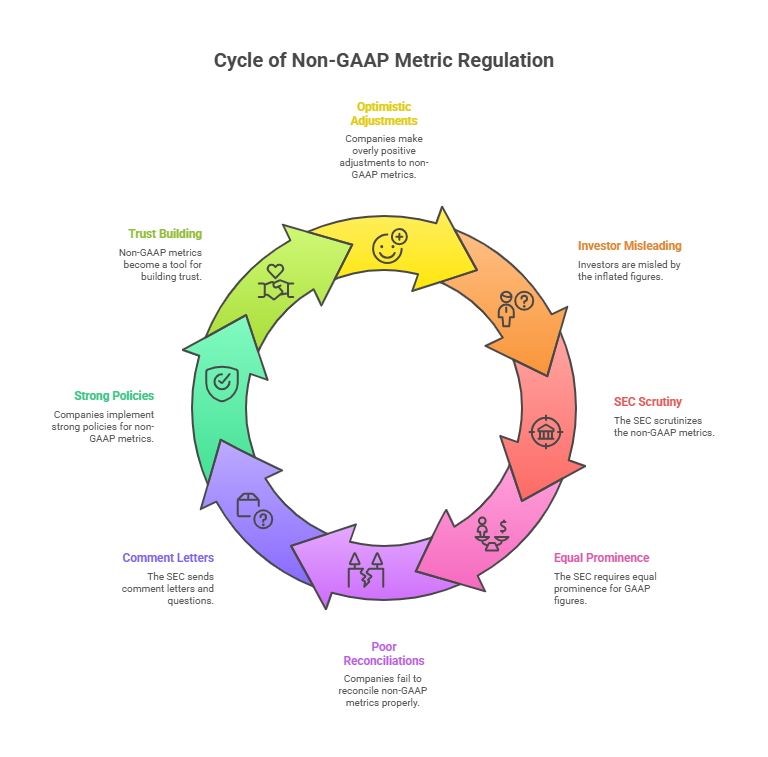

The SEC has recently focused on Non-GAAP abuses, requiring these measures to be transparent, reconciled with GAAP, and not presented more prominently than GAAP figures, as per regulations like Regulation G, Item 10(e) of Regulation S-K, and updated C&DIs.

Recent SEC actions and staff speeches highlight specific areas of concern:

- “Individually tailored” accounting that effectively rewrites GAAP (for example, recognizing revenue on a basis inconsistent with ASC 606 in a Non-GAAP metric).

- Cherry-picking adjustments – excluding recurring expenses while keeping recurring income.

- Undue prominence –putting GAAP in the footnotes and a Non-GAAP number in the headlines or tables.

When Non-GAAP Measures Add Value – and When They Don’t

Non-GAAP measures tend to be most valuable when they are:

- Well-defined and consistently applied over time

- Symmetrical (they modify not just “bad news,” but also income and expenses as necessary)

- Anchored in the economics of the business (e.g., removing clearly non-recurring items to focus on core operations)

- Clearly reconciled to GAAP, with each adjustment’s justification provided in simple terms

They become problematic when they are:

- Used to mask deteriorating GAAP performance

- Constantly changing definitions, making period-to-period comparisons impossible

- Filled with modifications that eliminate regular, ongoing expenses like payroll, marketing, or stock-based compensation

Key Regulatory Expectations (U.S. Perspective)

Under Regulation G and Item 10(e) of Regulation S-K, the SEC expects public companies that present non-GAAP measures to:

- Present GAAP measures with equal or greater prominence (e.g., GAAP EPS should not be overshadowed by Adjusted EPS).

- Provide a clear reconciliation from GAAP to Non-GAAP figures, with all material adjustments listed.

- Avoid misleading adjustments, such as:

- Reversing normal, recurring operating expenses to increase “adjusted” income.

- Reversing normal, recurring operating expenses to increase “adjusted” income.

- Creating revenue metrics that ignore GAAP’s timing principles (individually-tailored revenue recognition).

The Role of CPA Firms and Outsourced Accounting Partners

For U.S. businesses especially growing companies, startups, and mid-market entities outsourced accounting and advisory teams play a critical role in Non-GAAP governance:

- Designing appropriate metrics

Assisting management in identifying which modifications are appropriate and which Non-GAAP measures accurately reflect business drivers. - Implementing controls over calculations

Ensuring that each Non-GAAP metric is calculated consistently, using documented logic and system-driven routines where possible. - Preparing reconciliations and narratives

Drafting reconciliations and MD&A-style explanations that are clear, accurate, and regulator-ready. - Monitoring regulatory updates

Ensuring that disclosures remain up to date by keeping the reporting team informed about new SEC C&DIs, comment-letter trends, and enforcement topics.

For U.S. CPA firms, having an offshore partner who understands both technical rules and practical reporting pressures can materially strengthen their clients financial communication.

Governance, Controls and Documentation

Non-GAAP measurements can no longer be regarded as “marketing numbers” produced outside of the finance control environment due to increased scrutiny. Among the best practices are:

- Written guidelines and definitions outlining the objective of each non-GAAP statistic as well as any permitted modifications

- Internal controls over data, calculations and disclosure, aligned with SOX-style control frameworks for public companies

- The audit committee is in charge of determining which Non-GAAP metrics are used externally, how they are computed, and how they are shown.

- Periodic back-testing: comparing Non-GAAP and GAAP trends to ensure that adjustments continue to make sense and don’t obscure risk or volatility

Strong governance helps companies withstand SEC comment letters, investor questions, and due diligence in transactions or capital raising.

How Kariwala & Co. LLP Adds Value

At Kariwala & Co. LLP, we assist American accounting firms and companies who use Non-GAAP metrics to present a more transparent performance narrative without going over regulatory red lines.

Our teams support you by:

- Standardising non-GAAP definitions and policies, aligned with SEC expectations and investor best practices.

- Building robust reconciliation templates that ensure every Non-GAAP measure is traceable back to GAAP figures.

- Running period-end Non-GAAP calculations and quality checks, so numbers are consistent across earnings releases, internal decks, and lender packages.

Keeping your finance team informed of emerging SEC focus areas around Non-GAAP so you can stay ahead of scrutiny not react to it.

We assist American companies and CPA firms in using Non-GAAP measurements as a reliable analytical tool rather than a compliance concern by fusing technical precision with transparent communication.

References:

U.S. Securities and Exchange Commission – Non-GAAP Financial Measures (Regulation G and related guidance).