The financial landscape is undergoing swift advancements, with cryptocurrency spearheading this evolution. However many American enterprises and Certified Public Accountant (CPA) firms continue to experience ambiguity regarding the proper methods for recording and reporting their digital asset portfolios.

What Is “Cryptocurrency” vs “Crypto assets Accounting”?

Cryptocurrency

A digital token that is fungible and protected by cryptography, recorded on a decentralized system like Bitcoin or Ethereum. From an accounting perspective, it is classified as an intangible asset that is not considered money.

Cryptoassets

This signifies the accounting standards, such as Ind AS or U.S. GAAP, that dictate the procedures for recognizing, valuing, displaying, and reporting these tokens.

- Under U.S. GAAP, crypto guidance is now codified in ASC 350-60 (ASU 2023-08).

- Under Indian GAAP (Ind AS) entities apply Ind AS 38 (Intangible Assets) or Ind AS 2 (Inventories) there’s no dedicated crypto standard yet.

Accounting Treatments: India vs United States

A. India (Ind AS)

Classification

- Most entities: Record crypto holdings as intangible assets (Ind AS 38).

- Broker-traders: Treat them as inventory (Ind AS 2) if held for trading.

Measurement & Subsequent Accounting

- Ind AS 38: Typically the cost model is applied, which involves deducting any impairment losses. Revaluation is only allowed when there is an active market.

- Ind AS 2: Broker traders can measure holdings at fair value less costs to sell with changes recognised in profit or loss.

- Presentation & Disclosures

- Disclose as per Ind AS 38/36/113 and Schedule III requirements:

- Profit/loss on crypto transactions.

- Advances or deposits related to crypto investments.

B. United States (U.S. GAAP)

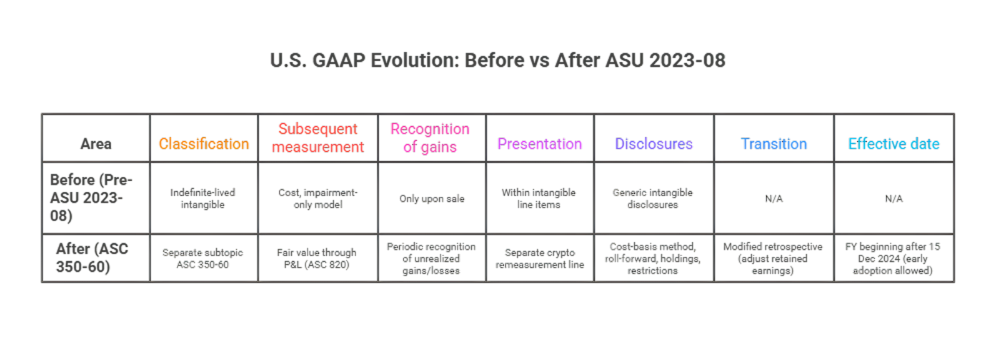

Before ASU 2023-08

Under ASC 350, cryptoassets were classified as indefinite-lived intangibles recorded at their cost minus any impairment. This accounting treatment prohibited upward revaluations, resulting in a “down-only” approach where value could only decrease.

After ASU 2023-08 → ASC 350-60 (Crypto Assets)

This new update effective for fiscal years beginning after December 15, 2024, introduces a fair-value model.

- Scope: Applies to fungible, cryptography secured digital tokens on a blockchain that are not issued by the entity and don’t provide enforceable rights.

- Measurement: Must be reported at fair value through net income (FVTNI) each period.

- Presentation: You’ll see crypto gains and losses listed separately from the usual amortization or impairment of other intangible assets.

- Disclosures: Entities must disclose cost basis methods, roll forward reconciliations, significant holdings, and restrictions on sale or transfer.

Illustrative Accounting Entries

Example Scenario:

A company holds 10 BTC purchased at $420,000. At year-end 2024, fair value = $500,000.

On adoption (Jan 1 2025):

- Dr Crypto Assets $80,000

- Cr Retained Earnings $80,000

Quarterly remeasurement (to $560,000):

- Dr Crypto Assets $60,000

- Cr Unrealized Gain (P&L) $60,000

Sale of 2 BTC at $124,000 total:

- Dr Cash $124,000

- Cr Crypto Assets $100,000

- Cr Realized Gain on Crypto $24,000

This demonstrates the fair value through the earnings model replacing the previous impairment only model.

Short-Term vs Long Term Gains on Cryptoassets

From an accounting not tax perspective:

Short Term Gains/Losses:

- Occur from frequent trading and fair value fluctuations recognized in net income.

- Affect P&L volatility and financial ratios.

Long Term Holdings:

- Impact balance sheet valuations and earnings per share due to cumulative fair value adjustments.

- Require consistent impairment testing and disclosure in Indian GAAP and periodic revaluation in U.S. GAAP.

Why These Differences Matter for U.S. Businesses

For U.S. CPA firms and financial controllers, these changes mean:

- Reporting that is more open and accurately reflects the economic situation.

- Volatility directly visible in earnings influencing performance metrics and valuation.

- There is a requirement for enhanced controls over asset valuation reconciliation of custodial assets and preparedness for audits.

For outsourced bookkeeping and accounting partners understanding both frameworks ensures seamless consolidation compliance and advisory for multinational clients holding crypto.

Kariwala & Co. LLP’s Expertise

At Kariwala & Co. LLP, we specialize in helping U.S. CPA firms and businesses understand and apply these complex accounting changes.

- We differentiate between Indian and U.S. standards to help clients maintain clarity in cross-border reporting.

- Our team sets up cryptoasset ledgers, ensures accurate fair-value measurement, and builds disclosure-ready reports aligned with ASU 2023-08.

- We train in-house finance teams on reconciling blockchain records with accounting systems, ensuring data integrity and transparency.

Conclusion

The FASB’s ASU 2023-08 marks a turning point in the accounting for digital assets replacing outdated impairment models with a fair-value approach that reflects true economic performance. While the U.S. has taken a clear step toward modernization, India’s accounting treatment remains principles-based relying on existing Ind AS guidance.

For businesses operating across both frameworks, clarity is essential. Kariwala & Co. LLP stands ready to simplify that complexity ensuring that your cryptoasset reporting remains accurate, compliant, and forward-looking in this evolving financial era.

Reference:

FASB — Projects page for “Accounting for and Disclosure of Crypto Assets”: fasb.org