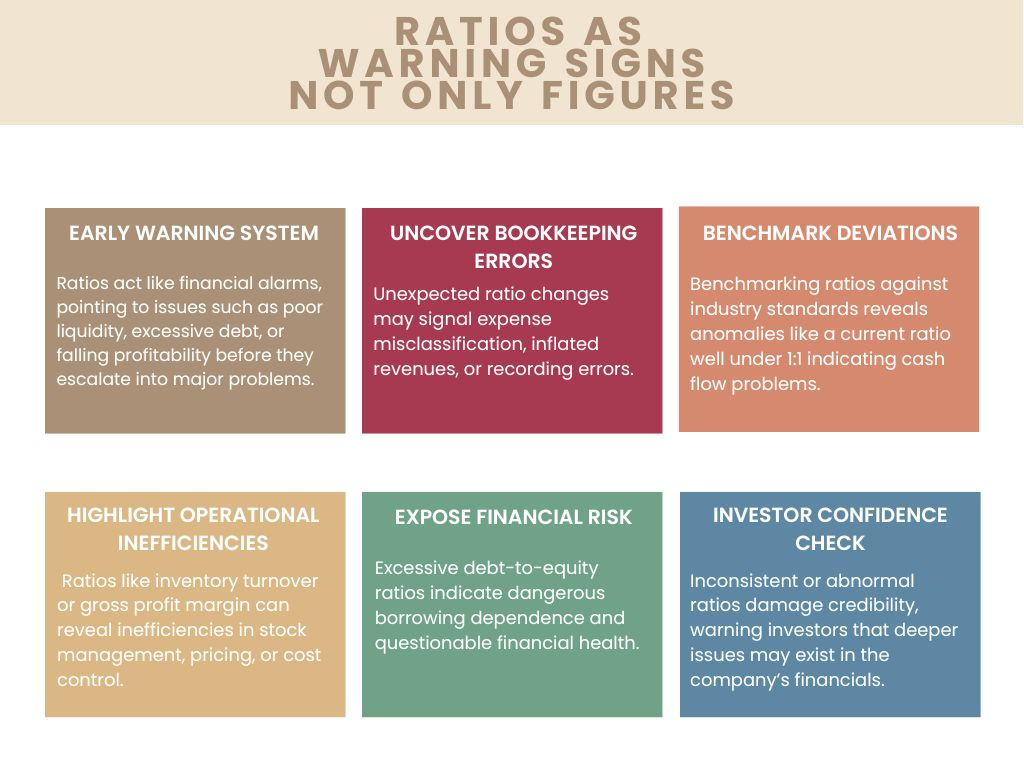

Accounting inaccuracies frequently remain undetected until they precipitate significant fiscal disturbances. Minor discrepancies in expenditure documentation, revenue inflation, or improper account categorization may obscure an organization’s authentic financial status. It is in this context that ratio analysis emerges as an invaluable instrument. Through the systematic examination of financial ratios, enterprise proprietors, accounting professionals, and stakeholders can expeditiously identify anomalies, uncover concealed inaccuracies, and verify that the financial records accurately represent the organization’s operational performance.

What is Ratio Analysis?

Ratio analysis constitutes a systematic methodology for assessing an organization’s financial documentation through the computation of proportional relationships among critical figures within the balance sheet, income statement, and cash flow statement. This analytical approach facilitates the transformation of unprocessed financial information into substantive and actionable intelligence.

The Significance of Ratio Analysis for Corporate Entities

Ratio analysis plays a critical role in corporate decision-making because:

- It detects errors: Unexpected fluctuations in ratios may signal mistakes in bookkeeping entries.

- It ensures accuracy: Consistent ratios over time confirm reliable financial reporting.

- It supports decision-making: Management can use ratios to track performance and identify problem areas.

How Ratio Analysis Links with Bookkeeping

Bookkeeping forms the foundation of ratio analysis. If transactions are recorded incorrectly, ratios will be misleading. For instance:

- When expenditures are reported below their actual values, financial performance metrics demonstrate artificially enhanced profitability that does not accurately reflect the organization’s true economic position.

- Excluding liabilities distorts solvency ratios, creating misleading financial stability indicators. Regular ratio analysis helps companies identify discrepancies quickly and fix accounting errors before they escalate into compliance problems or damage investor confidence.

Why Bookkeeping is the Backbone of Ratio Analysis

Accuracy of Data

Ratios are only as good as the numbers behind them. If sales, expenses, or liabilities are wrongly entered, every ratio becomes misleading, and decisions based on them turn risky.

Consistency Over Time

Proper bookkeeping ensures transactions are recorded in the same way each period. This makes ratio trends reliable and helps companies compare performance year over year.

Early Error Detection

Small bookkeeping mistakes — like duplicate entries or missed invoices — get exposed through ratios. Clean records make these errors visible sooner, before they snowball into compliance or cash flow problems.

Investor and Lender Confidence

Well-maintained books keep ratios trustworthy, which reassures investors, auditors, and banks. Without accurate bookkeeping, even strong ratios lose credibility in the eyes of stakeholders.

Strategic Decision Support

When bookkeeping is precise, ratios truly reflect business health. This allows management to plan expansion, manage debt, or adjust pricing with confidence that their numbers aren’t distorted.

The Principal Categories of Financial Ratios:

There are several financial ratios, but companies primarily rely on five key ratios to assess health and detect hidden errors.

1. Current Ratio (Liquidity)

Formula: Current Assets ÷ Current Liabilities

Ideal Benchmark: 2:1

The current ratio tells us if a company can pay its short-term debts with short-term assets like cash, receivables, and inventory. A ratio below 2:1 suggests tight liquidity and possible trouble meeting obligations. A ratio well above 2:1 can mean assets are lying idle without being invested productively.

From a bookkeeping standpoint, minor inaccuracies such as undocumented vendor invoices or omitted accounts receivable can render this ratio deceptive. Preserving precise record-keeping guarantees that this ratio accurately represents the organization’s genuine financial stability, upon which creditors and stakeholders place considerable emphasis when evaluating fiscal soundness.

2. Debt-to-Equity Ratio (Leverage)

Formula: Total Debt ÷ Shareholders’ Equity

Benchmark: < 1:1 conservative; 1–2:1 moderate; > 2:1 risky

This metric demonstrates the extent to which an organization relies upon external financing relative to equity capital. An elevated ratio indicates substantial leverage, thereby increasing the organization’s susceptibility to liquidity challenges should borrowing costs escalate. Conversely, a diminished ratio signifies fiscal prudence and stability, though it may concurrently indicate foregone expansion prospects.

From a bookkeeping perspective, misclassification of loans (short-term vs. long-term) or missing accrued interest can distort this ratio. Proper recording ensures clarity on how much of the company’s operations are financed through external borrowing versus internal funds.

3. Gross Profit Margin (Profitability)

Formula: (Revenue − COGS) ÷ Revenue × 100

Benchmark: 20%–40% for many industries (varies by sector)

The gross margin demonstrates the effectiveness with which an organization converts direct expenses into income. An abrupt increase in margin may indicate inflated revenue figures or inadequately reported expenditures. A significant decline might reflect escalating expenses that have not been comprehensively documented.

Accurate bookkeeping of both sales and direct costs is essential here. For businesses, this ratio is the first checkpoint of financial health — a distorted margin gives management the wrong impression of profitability and can lead to poor pricing, budgeting, and investment decisions.

4. Inventory Turnover (Efficiency)

Formula: COGS ÷ Average Inventory

Benchmark: Retail 5–10×/year; Manufacturing 3–6×/year

This ratio reveals how quickly inventory is sold and replaced. A very high turnover could mean inventory is undervalued in the books. A very low turnover might suggest overstocking, obsolete items, or inflated inventory balances.

Because inventory entries involve valuation, timing, and adjustments, bookkeeping accuracy is crucial. Errors here don’t just distort this ratio — they ripple across profit margins, cash flow, and working capital. Companies use this ratio to plan procurement, avoid dead stock, and manage cash efficiently.

5. Return on Equity (ROE — Shareholder Returns)

Formula: Net Income ÷ Shareholders’ Equity × 100

Benchmark: 10–20% is healthy; >20% strong (but often linked to high leverage)

Return on Equity serves as an indicator of an organization’s proficiency in utilizing shareholder capital to produce earnings. When net earnings are artificially elevated or shareholder equity is inadequately represented, the ROE metric may present a more favorable appearance than the actual financial performance, thereby creating potential misrepresentation for both executive leadership and stakeholders.

Accurate bookkeeping ensures the “bottom line” reflects true earnings. For investors, ROE is a key performance indicator; for management, it confirms whether strategies are yielding value or draining resources.

Spotting Mistakes Through Ratios

Here’s how ratio analysis helps catch “sneaky” bookkeeping issues:

- Inflated revenues → Gross Profit Margin spikes without matching sales growth.

- Missing liabilities → Current Ratio appears healthier than reality.

- Inventory errors → Turnover ratio shows unrealistic efficiency or sluggishness.

- Debt misreporting → Debt-to-Equity ratio doesn’t align with industry averages.

How Small Businesses Can Use Ratios Effectively

- Keep it Simple – Focus on 4–5 key ratios rather than trying to calculate everything.

- Integrate with Month-End Closing – Make ratio checks part of the monthly closing checklist.

- Leverage Dashboards – Many accounting systems now provide real-time ratio insights.

- Seek Expert Review – A CPA or outsourced accounting partner can interpret ratios with more depth.

Conclusion

Ratio analysis transcends its fundamental role as a financial assessment methodology, serving as a critical protective mechanism against concealed accounting irregularities. Through systematic examination of financial ratios and their comparison to established industry standards, organizations can maintain precision in their financial reporting, preserve stakeholder confidence, and enhance the quality of their strategic financial decision-making processes. At Kariwala & Company LLP, we help small businesses and CPA firms leverage ratio analysis to uncover financial red flags early, strengthen compliance, and maintain confidence in their numbers. With the right ratios, your books tell the real story, not a distorted one.