Revenue is a key performance metric in U.S. businesses, directly impacting profitability, valuation, investor confidence, and regulatory compliance.Errors in revenue recognition, whether intentional or procedural, present significant risks to financial reporting.

Under U.S. GAAP (ASC 606), revenue must be recognized when performance obligations are satisfied and control is transferred, not merely when cash is received. Noncompliance can result in misstated financial statements, regulatory scrutiny, audit findings, and diminished valuation.

What This Topic Really Means

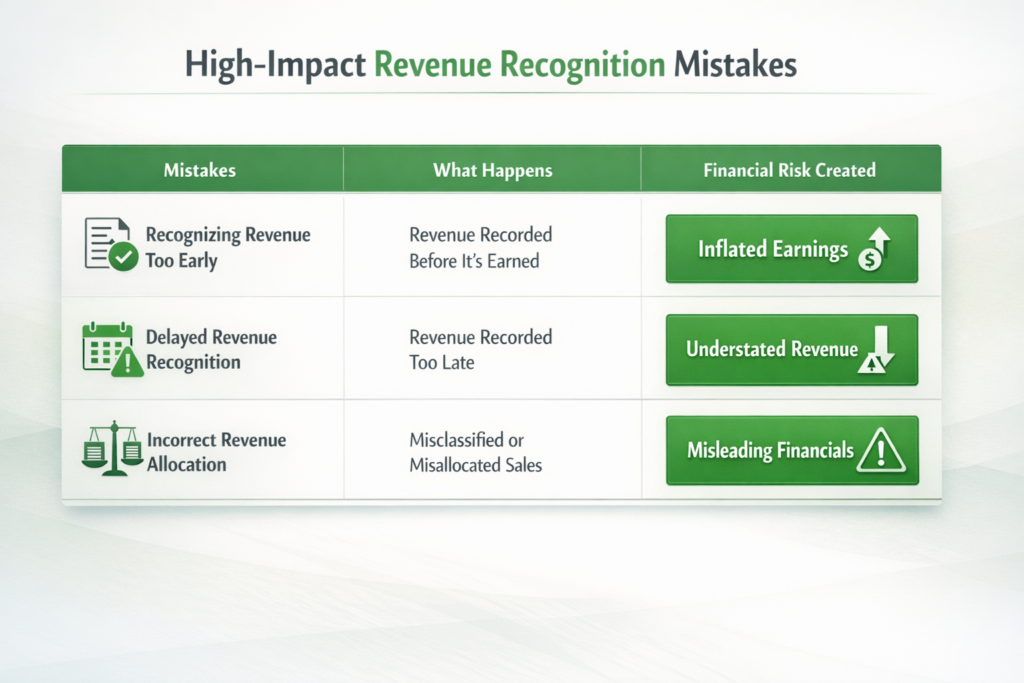

Improper revenue recognition includes:

- Recording revenue prematurely

- Delaying revenue recognition

- Misclassifying revenue streams

- Recognizing revenue without fulfilling performance obligations

- These practices result in financial statements that do not accurately reflect the economic reality of the business.

Behavioral Red Flags Inside Organizations

Improper revenue recognition is often driven not only by technical gaps but also by behavioral factors.

Common internal patterns include:

- Pressure to meet quarterly financial targets

- Lack of coordination between sales and accounting teams

- Overreliance on manual adjustments

- Weak internal control review processes

- These behaviors increase the likelihood of both intentional and unintentional misstatements.

The Real Problem: Timing vs. Economic Reality

At its core, improper revenue recognition is a timing issue:

- Early billing

- Business practice: Recognize immediately

- U.S. GAAP requirement: Recognize when earned

- Advance payments

- Business practice: Treat as revenue

- U.S. GAAP requirement: Record as liability

- Long-term contracts

- Business practice: Recognize upfront

- U.S. GAAP requirement: Recognize over time

- Bundled services

- Business practice: Lump sum recognition

- U.S. GAAP requirement: Allocate across obligations

- The disconnect between cash flow and revenue recognition is the underlying cause of most reporting risks.

The 5 Step Revenue Recognition Model (U.S. GAAP – ASC 606)

Businesses are required to follow a structured framework:

- Identify the contract with a customer

- Identify performance obligations in the contract

- Determine the transaction price

- Allocate the transaction price to performance obligations

- Recognize revenue when performance obligations are satisfied

Stakeholder Impact Breakdown

1. Business Owners

- Improper revenue recognition creates a misleading view of growth

- Leads to flawed strategic decisions

- Results in potential future corrections

2. Investors and Buyers

- Increases perceived risk

- Often results in:

- Lower valuation multiples

- Extended due diligence timelines

- Deal renegotiations

3. CPA Firms and Auditors

- Increases audit complexity

- Requires:

- Additional testing procedures

- Revenue restatements

- Enhanced compliance reporting

High Impact Revenue Recognition Mistakes

Advanced Risk Scenarios

- Multi-Element Arrangements

Bundled service offerings often create challenges in properly allocating revenue across performance obligations. - Variable Consideration

Discounts, incentives, and rebates are frequently overlooked, resulting in overstated revenue. - Contract Modifications

Contract changes are not consistently updated in accounting systems, leading to reporting inconsistencies. - Cutoff Errors

Revenue recognized in the incorrect period remains one of the most common audit findings in the United States.

How to Fix and Prevent Revenue Recognition Errors (Step-by-Step)

Step 1: Standardize Contracts

Ensure all contracts clearly define deliverables and payment terms.

Step 2: Apply ASC 606 Consistently

Train teams to rigorously follow the five-step revenue recognition model.

Step 3: Automate Revenue Tracking

Implement accounting systems that align revenue recognition with performance obligations.

Step 4: Perform Monthly Reviews

Conduct regular reviews of revenue entries and reconciliations.

Step 5: Maintain Documentation

Retain complete audit trails for all revenue transactions.

Case Insight

A U.S.-based SaaS company recognized annual subscription revenue upfront instead of over the subscription period.

Issue:

Revenue was overstated by 25%

Action Taken:

Revenue was restated in accordance with ASC 606

Financial statements were corrected

Result

Initial valuation declined

Transaction was delayed but ultimately completed after correction

Why This Matters for Business Valuation

Revenue serves as the foundation for EBITDA and valuation multiples. When revenue is overstated:

1.EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) becomes unreliable

2.Buyers apply valuation discounts

3.Transactions may fail during due diligence

In many U.S. transactions, revenue-related adjustments are among the primary drivers of valuation reductions.

Conclusion

Accurate revenue recognition reflects true business performance. Improper practices introduce hidden risks that impact financial reporting, investor confidence, and valuation. A disciplined, GAAP compliant approach to revenue recognition builds a strong financial foundation for sustainable growth.

References:

Financial Accounting Standards Board (FASB)

ASC 606: Revenue from Contracts with Customers

Core framework for revenue recognition in the United States

Link: