Introduction:

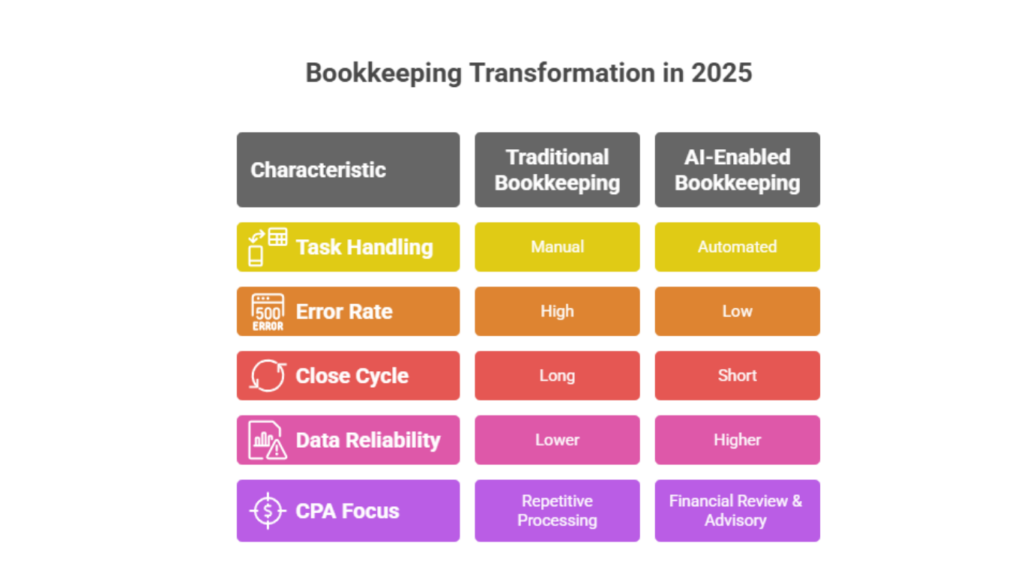

By the year 2025, bookkeeping practices in the United States have advanced significantly beyond simple manual reconciliation and automated processes based on fixed rules. Artificial intelligence has become an integral part of everyday accounting tasks, not to substitute Certified Public Accountants CPA’s but rather to enhance their productivity and improve accuracy. CPA firms across the U.S. are progressively implementing AI-powered bookkeeping systems to manage increasing transaction volumes, meet accelerated reporting deadlines, address heightened compliance requirements, and satisfy client needs for immediate financial data.

What AI-Driven Bookkeeping Really Means in Practice

AI-driven bookkeeping is not about “robots doing accounting.” Instead it refers to intelligent systems that learn from historical data, recognize patterns, and assist accountants in decision making.

Unlike traditional automation tools that follow fixed rules, AI systems:

- Continuously improve with usage

- Detect anomalies that humans may miss

- Adapt to changing transaction behavior

For U.S. CPA’s this means bookkeeping systems that actively support accuracy, compliance, and advisory work rather than simply recording data.

Shift from Data Entry to Financial Oversight

American CPA firms are shifting from bookkeeping models that rely heavily on entry-level staff to workflows centered on review processes. The standardization of routine recording tasks is enabling professionals to dedicate more effort to verifying financial data, spotting discrepancies, and offering clients guidance on cash flow and performance patterns.

This shift improves quality control and reduces dependency on repetitive manual work, especially during month-end and year-end closes.

Key Areas Where U.S. CPAs Are Using AI in 2025

1. Intelligent Transaction Classification

AI automates transaction categorization in bookkeeping. By analyzing vendor behavior, past coding, descriptions, amounts, and timing, AI systems accurately classify transactions in 2025. Unlike older systems needing frequent rule changes, modern AI learns continuously, improving accuracy over time. This saves CPA firms review time and ensures consistency for clients, especially those with many transactions.

2. Continuous Bank and Credit Card Reconciliation

AI has transformed reconciliation from a month end task into a continuous process:

- Real-time matching of bank feeds with ledger entries

- Identification of missing, duplicated, or unmatched transactions

- Automated suggestions for corrections

- Early detection of reconciliation discrepancies

This approach allows CPAs to identify issues earlier in the cycle rather than discovering problems weeks later.

3. Exception-Based Review Model

U.S. CPA firms in 2025 are increasingly shifting to an exception based bookkeeping model, where humans focus only on what truly needs attention:

- AI processes and reviews 100% of transactions

- Normal, low risk entries pass through automatically

- High-risk or unusual items are flagged

- Accountants review only flagged exceptions

This model significantly improves productivity while preserving professional judgment where it matters most.

4. AI-Driven Error and Anomaly Detection

Modern AI bookkeeping tools continuously monitor patterns in transaction frequency, amounts, vendors, and posting behavior. When unusual deviations occur such as sudden expense spikes, duplicate invoices or irregular timing the system alerts the accountant.

For CPAs, this reduces downstream audit issues and strengthens internal controls, especially for clients preparing for reviews, audits or investor reporting.

5. How Automated Invoice Handling Improves Day-to-Day Bookkeeping

AI tools now extract data from invoices, receipts, and statements, validate them against past records, and post entries with minimal human intervention.

Day-to-Day Bookkeeping Workflow in a Modern CPA Firm

- Transaction recording using standardized accounts

- Daily or weekly internal checks

- Periodic reconciliations (bank, AR, AP)

- Supervisor-level review and adjustments

- Client-ready financial reporting

This structure helps firms reduce errors while maintaining control at every stage.

Why CPA Firms Are Repositioning Bookkeeping as a Value Service

Bookkeeping is increasingly positioned as the foundation for advisory services. Clean, timely books allow CPAs to offer budgeting insights, cash flow forecasting, and performance reviews. Firms that recognize this are gaining stronger client relationships and recurring revenue.

AI-Driven Controls: Strengthening Accuracy and Compliance in Bookkeeping

Modern AI bookkeeping systems embed intelligent controls into daily operations. These systems flag duplicate entries, unusual transactions, vendor data errors, and policy violations before impacting financial statements. For U.S. CPA’s this means better internal review, stronger audit trails, and greater confidence in financial reporting. AI controls also help comply with evolving U.S. accounting standards by maintaining consistent, auditable data records.

Conclusion

AI-driven bookkeeping in 2025 reflects a fundamental shift in how U.S. CPA’s operate. By automating routine work, improving accuracy, and unlocking real-time insights, AI allows accounting professionals to focus on higher value analysis and advisory. The future of bookkeeping is not just automated it is intelligent, proactive, and CPA led.

Reference:

Journal of Accountancy (AICPA) – AI applications in bookkeeping and accounting