Businesses today emphasize automation, dashboards, and real time reporting. However, a hidden layer, shadow accounting, often develops beneath these systems. It is not in official statements or audits, yet it impacts decisions, skews reports, and raises risk. Often unintentional, it starts as workarounds like spreadsheets or offline trackers, growing into unmonitored parallel systems.

Understanding Shadow Accounting through a Practical Lens

Shadow accounting is best understood not as a technical flaw, but as an operational workaround.

It appears when:

- Financial systems cannot fully capture real time business activity

- Teams feel the need to adjust numbers for internal understanding

- Reporting timelines do not match decision making speed

Over time, these workarounds evolve into independent financial ecosystems that exist parallel to official books.

A Different Perspective: Is It Always a Problem?

Let’s challenge the assumption.

Shadow accounting, in its early stages, actually reflects:

- A need for greater flexibility

- A gap in system usability

- A demand for faster insights

This means shadow accounting is not just a risk, It is also a signal. A signal that your financial systems are not fully aligned with business needs.

Why Shadow Accounting Exists:

A – Accessibility Issues

Teams often lack real time access to accounting systems, leading them to create parallel trackers.

B – Business Complexity

Growing organizations struggle to align operational data with financial reporting structures.

C – Control Gaps

When internal controls are weak or unclear, employees rely on their own tracking mechanisms.

D – Data Trust Deficit

If official reports are perceived as delayed or inaccurate, departments build their own trusted numbers.

E – Efficiency Pressure

Quick decision making demands instant insights something formal accounting systems do not always provide.

In the U.S. Accounting industry, this issue is becoming increasingly common due to:

🔹 Remote working environments

🔹 Multiple departments handling financial data

🔹 Rapid business scaling

🔹 Dependency on spreadsheets

🔹 Lack of process standardization

🔹 Complex revenue recognition requirements

🔹 Multi-platform business operations

Shadow Accounting burdens outsourced accounting firms and finance professionals, as teams waste time reconciling unofficial records with actual books. This prevents them from focusing on strategic financial analysis, trapping them in spreadsheet error correction and disconnected report reconciliation.

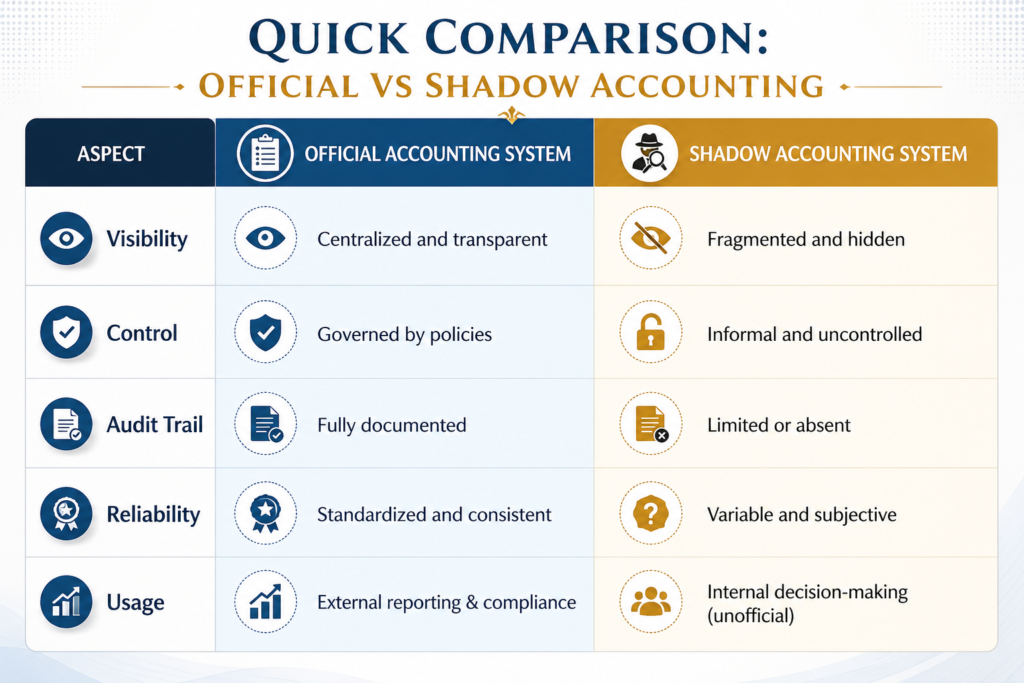

A Quick Comparison: Official vs Shadow Accounting

A Silent Threat to the U.S. Businesses

In the U.S. regulatory environment especially under frameworks like GAAP and SOX compliance transparency and control are critical.

Shadow accounting directly undermines:

- Audit readiness

- Internal control frameworks

- Data integrity standards

- Stakeholder confidence

For CPA firms and finance leaders, this is not just an operational issue it is a governance risk.

From Risk to Control: How Leading Firms Are Addressing It

Rather than forcing immediate elimination, leading organizations focus on integration and alignment.

Strategic approach includes:

- Strengthening ERP capabilities to match operational needs

- Creating real time reporting dashboards accessible across teams

- Standardizing data definitions across departments

- Enhancing internal controls without slowing operations

- Building trust in finance through transparency and collaboration

The goal is not to remove flexibility but to bring all financial activity into a controlled, auditable environment.

Decoding the Root Causes

C – Complexity Growth

Business expansion outpaces system capabilities

A – Access Limitations

Teams do not have real time visibility into financial data

U – Unstructured Processes

Lack of standardized workflows across departments

S – System Rigidity

ERP systems fail to adapt to operational nuances

E – Expectation Gap

Management expects faster insights than systems can deliver

The Hidden Risks: More Than Just Data Duplication

| Risk Area | Impact on Business | Long Term Consequence |

| Financial Reporting | Misaligned numbers across departments | Inaccurate financial statements |

| Compliance & Audit | Untracked adjustments and undocumented entries | Audit qualifications or regulatory scrutiny |

| Decision Making | Conflicting data sources | Poor strategic decisions |

| Internal Controls | Bypassed approval and validation processes | Increased fraud or error risk |

| Operational Efficiency | Time wasted reconciling multiple data sources | Reduced productivity and higher costs |

Why It Matters for CPA Firms and Outsourcing Partners

For CPA firms serving U.S. clients, shadow accounting presents a unique challenge:

- Reported numbers may not reflect actual operations

- Client provided data may be incomplete or inconsistent

- Audit trails may be fragmented

Outsourcing partners, especially those working across time zones, play a crucial role in:

- Identifying inconsistencies early

- Standardizing reporting structures

- Ensuring alignment between operational and financial data

- Supporting clean, audit ready books

The Kariwala Perspective: Turning Risk into Opportunity

At Kariwala & Co. LLP, shadow accounting is not viewed merely as a compliance gap it is an opportunity to strengthen financial architecture.

By aligning systems, processes, and people, businesses can:

- Eliminate duplicate data streams

- Improve reporting accuracy

- Enhance decision making confidence

- Achieve faster and cleaner financial closes

Most importantly, they can ensure that every financial decision is based on a single, reliable version of truth.

improves operations, reporting, and decision making, as strong businesses depend on reliable data.