A Long Ignored Accounting Gap Is Finally Closing

For years, US accounting rules lacked clarity on how businesses should account for government grants. This led to varied practices, with companies using international standards, nonprofit models, or their own internal policies for state incentives, subsidies, and funding. Consequently, financial reporting was inconsistent. However, the FASB has now introduced formal guidance (ASC 832 via ASU 2025-10), establishing an official framework for these grants.

This change significantly impacts how businesses recognize, present, disclose, and manage government assistance in their financial statements.

Why This Topic Matters More Than Ever

Government assistance has grown rapidly in recent years due to:

- Infrastructure investments

- Clean energy initiatives

- Semiconductor manufacturing incentives

- Training programs for workers

- State level tax and employment grants

- Programs to help things get back to normal after COVID

Businesses across the US are increasingly relying on government backed programs to fund expansion and operations.

However, investors, auditors, lenders, and regulators need transparency regarding:

- How grants are recorded

- When grant income is recognized

- Whether conditions attached to grants are being met

- How dependent companies are on government support

This new accounting framework directly addresses these concerns.

What Exactly Is a Government Grant?

Under the new framework, a government grant generally refers to:

A transfer of cash or tangible nonmonetary assets from a government to a business entity where the transaction is not considered a normal exchange transaction.

Examples include:

- Manufacturing incentives

- Hiring subsidies

- Clean energy reimbursements

- Land grants

- Equipment grants

- Research funding

- Economic development incentives

- Relocation assistance

The guidance mainly applies to for-profit business entities.

Real World Example

Imagine a US manufacturing company receives a $5 million state grant to expand operations and create 300 jobs over three years.

Earlier, companies may have treated this differently:

- Some recognized income immediately

- Some deferred recognition

- Some matched it against expenses

Under the newer structured approach:

The company must evaluate:

- Are employment targets achievable?

- Are all grant conditions being satisfied?

- Is repayment possible if targets fail?

- Over what period should the benefit be recognized?

This creates more disciplined financial reporting.

Key Features of the New Government Grant Framework

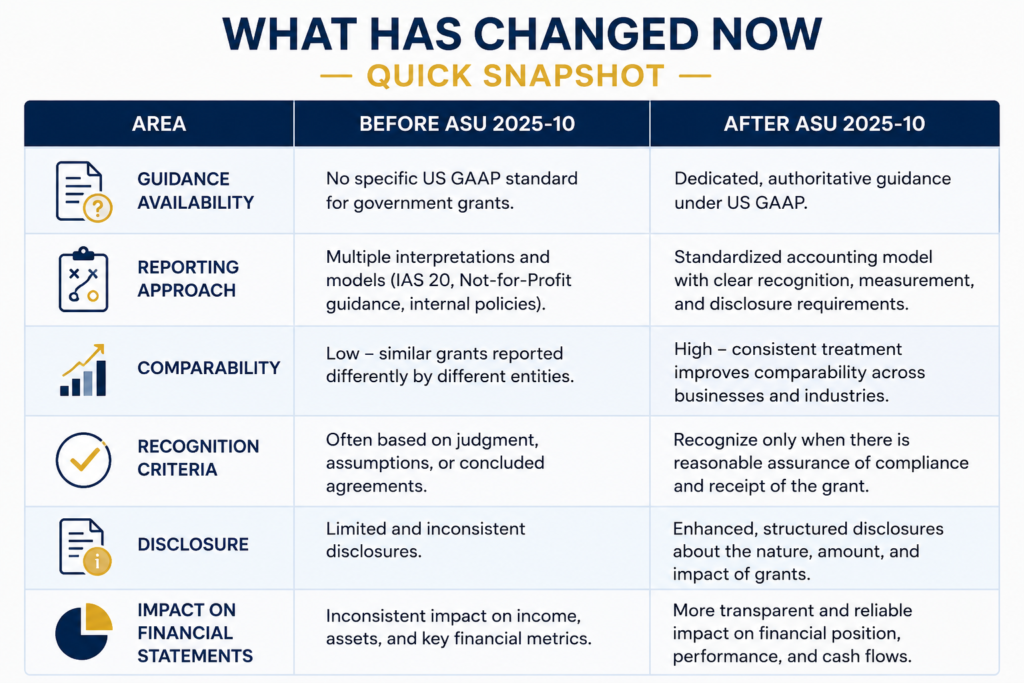

1. Formal Recognition Criteria

A grant is recognized only when:

- Compliance with grant conditions is probable

- Receipt of the grant is probable

This reduces premature income recognition.

2. Asset Grants vs Income Grants

A. Grants Related to Assets

These are grants connected to:

- Buildings

- Machinery

- Production equipment

- Infrastructure assets

These grants are typically recognized over the useful life of the asset.

B. Grants Related to Income

These grants relate to:

- Payroll support

- Employee retention

- Research funding

- Operating reimbursements

- Training programs

These are generally recognized over the period in which related expenses occur.

3. Stronger Disclosure Requirements

Companies will now need to disclose:

- Nature of the grants

- Accounting policies applied

- Significant terms and conditions

- Outstanding contingencies

- Unfulfilled obligations

- Presentation methods

This improves investor confidence and financial statement clarity.

Why CPA Firms and Accounting Teams Must Prepare Early

Accounting professionals will play a critical role in helping companies:

- Examine grant contracts

- Identify performance obligations

- Determine recognition timing

- Build compliant documentation

- Assess disclosure requirements

- Compile comprehensive audit support documentation

This is especially important because many companies currently maintain inconsistent internal grant accounting practices.

What Has Changed Now:

Hidden Operational Challenges Companies May Face

Businesses often prioritize grant funding over its accounting challenges. Grants frequently include conditions like employment minimums, operational promises, geographic restrictions, sustainability goals, or reporting duties. Neglecting to monitor these can lead to financial corrections, repayment risks, or audit issues. New guidelines compel companies to improve collaboration between finance, operations, legal, and compliance departments. Government grants are now significant accounting matters, not just operational benefits.

What This Means for Outsourced Accounting and Bookkeeping Firms

For firms providing outsourced accounting services to US clients, this change creates a significant opportunity.

Clients may increasingly require support for:

| Service Area | Potential Demand |

| Grant tracking | Higher |

| Compliance reporting | Higher |

| Deferred income schedules | Higher |

| Audit support documentation | Higher |

| Disclosure preparation | Higher |

| Month-end reconciliation | Higher |

| Grant condition monitoring | Higher |

Firms that understand evolving US GAAP requirements will become more valuable strategic partners.

Conclusion

As government incentives grow in manufacturing, clean energy, infrastructure, and technology, accounting for them must become consistent. Formalizing US GAAP for government grants modernizes financial reporting. Early adopters will improve compliance, transparency, audit readiness, and stakeholder trust. This change also creates new advisory and compliance service opportunities for accounting professionals and firms.