Recent U.S. government reviews, regulatory briefings, and agency observations during 2024–25 have made one point clear: supply chain disruptions are no longer just operational issues, they are accounting and financial reporting risks. From inventory valuation errors to disclosure failures and forecasting distortions, supply chain instability is now directly impacting how U.S. companies prepare, audit, and rely on their financial data.

This shift has major implications for CFOs, CPAs, controllers, auditors, and offshore accounting teams supporting U.S. businesses.

Why CPA Firms Cannot Ignore Supply Chain Risks Anymore

Recent U.S. government reports from 2024–25, issued by entities like the GAO, SEC, and PCAOB, have unequivocally demonstrated that disruptions in supply chains now pose a significant financial reporting and auditing risk, extending beyond mere operational concerns. Consequently, accounting firms are facing growing expectations to pinpoint, assess, and address the accounting implications stemming from supply chain volatility. For CPA firms that cater to businesses involved in manufacturing, distribution, retail, or import reliant operations, these risks are now surfacing directly within audit conclusions, client financial assessments, and consulting projects.

Mistakes in inventory valuation can directly expose CPA firms to audit risks

Supply chain disruptions have caused volatile material costs, freight surcharges, and supplier price resets. CPA firms are now encountering inventory balances that fail LCM, NRV, or impairment tests.

How CPA firms are affected

- Increased audit adjustments and post close corrections

- Higher risk of inventory overstatement findings

More time spent defending valuation assumptions with regulators and lenders

How CPA firms can resolve this

CPA firms should lead clients toward:

- Periodic inventory remeasurement (not annual only testing)

- Clear valuation policies aligned with ASC 330

- Documented assumptions supporting management estimates

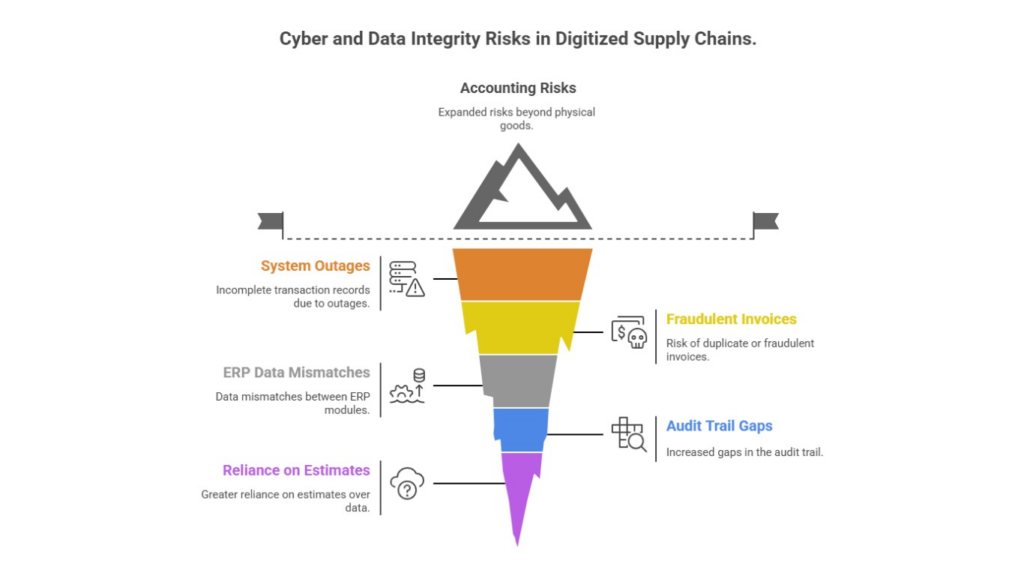

Key Supply Chain Accounting Risk Areas Identified by U.S. Authorities (2024–25)

In 2024–25, U.S. government and oversight reports indicate that supply chain disruptions primarily manifest as accounting risks via issues with inventory valuation, inconsistent cost assignments, untrustworthy vendor information, delayed recording of expenses, and compromised financial projections. These vulnerabilities significantly impact an organization’s preparedness for audits, the precision of its financial statements, and the effectiveness of management’s strategic choices, thereby becoming a paramount concern for accounting departments and CPA firms assisting American enterprises.

Working Capital Stress: A Hidden Accounting Exposure

| Supply Chain Issue | Accounting Impact | Business Consequence |

| Over-stocking to avoid shortages | Higher inventory carrying value | Cash flow pressure |

Delayed supplier deliveries | Accrued liabilities misaligned | Vendor disputes |

| Advance payments to suppliers | Prepaid expense complexity | Liquidity risk |

| Slow-moving inventory | Higher write-down risk | Reduced ROA |

Regulatory Scrutiny Is Expanding CPA Responsibilities

The PCAOB and SEC have increased attention on supply chain related audit risks.

CPA firm implication

- Expanded audit scope

- Higher documentation standards

- Greater professional judgment exposure

Firm-level response

Standardizing audit programs around supply chain risks and enhancing staff training is now essential.

Disclosure & Going Concern Pressure on CPA Firms

U.S. regulators now expect enhanced disclosures around supply chain dependency.

CPA firm challenge

- Determining when supplier concentration becomes a material risk

- Evaluating disclosure adequacy under SEC scrutiny

- Aligning footnotes with actual financial exposure

How CPA firms add value

By guiding clients on:

- Risk focused disclosures

- Dependency analysis

- Consistency between MD&A and financial statements

This strengthens both compliance and investor confidence.

Disclosure Expectations Are Rising

The SEC has emphasized transparency around supplier concentration and supply chain dependency. This aligns with disclosure guidance discussed in the Journal of Accountancy.

CPA responsibility

Firms must evaluate:

- Whether supply chain risk is material

- Adequacy of footnote disclosures

- Consistency between MD&A narratives and financial data

This has expanded the CPA’s role from preparer to risk evaluator.

Why This Matters to Offshore Accounting Teams

While India has not issued a single consolidated supply chain accounting report like the U.S., Indian professionals supporting U.S. clients are directly impacted. Offshore accounting teams must:

- Adjust inventory and cost models quickly

- Support enhanced audit documentation

- Track supplier-related cost changes accurately

- Help U.S. firms meet rising disclosure expectations

For Indian accounting partners, understanding U.S. supply chain risk narratives has become essential, not optional.

Conclusion

Supply chain instability is a 2024-25 U.S. government reporting concern, impacting financial reporting beyond logistics. Businesses with misaligned accounting face increased audit risk, poor forecasts, and diminished stakeholder trust. CPA firms and accounting teams can help clients manage supply chain uncertainty for better financial clarity and control.

Reference:

U.S. Government Accountability Office (GAO) – Supply Chain Risk Management Reports