Inventory in manufacturing is essentially frozen cash, often comprising 40-60% or more of a company’s assets, including raw materials, work-in-progress, finished goods, and spare parts. Errors in inventory accounting negatively impact cost of goods sold, gross margin, pricing, tax calculations, loan agreements, and management decisions. This article explores common manufacturing inventory accounting issues, their causes, and solutions through disciplined processes and expert outsourcing.

Wrong Categorisation of Inventory (Raw Material, WIP, Finished Goods)

One of the most common problems in manufacturing is misclassification:

- Raw materials booked as WIP or finished goods still shown as WIP.

- Items issued to production physically but not recorded in the system.

- Returned goods from customers wrongly treated as fresh finished goods.

This leads to overstated or understated inventory and incorrect COGS.

How it’s resolved:

- Clear definitions and policies for each category (RM, WIP, FG).

- Standard issue and return procedures linked to production orders.

- Periodic reconciliation between production reports and inventory ledger.

Weak Controls over Cutting, Issuance & Fabric Utilization

Cutting departments often operate without robust real-time tracking of marker efficiency, fabric yield, or residual scraps. Decisions taken manually on the production floor translate into losses that are not recorded in books. Weak controls cause invisible waste, inaccurate standard cost benchmarking, and poor cost recovery during costing and pricing.

Inaccurate Bills of Material and Routing Data

Issue | Operational Impact | Financial Consequence |

Missing components | Production stoppage | Urgent purchase premiums |

Incorrect quantities | Excess scrap | Higher COGS |

Outdated routing times | Incorrect labor costing | Margin compression |

Engineering changes untracked | Frequent rework | Write-offs |

Accurate BOM and routing data are foundational for stable costing, scheduling, and inventory valuation.

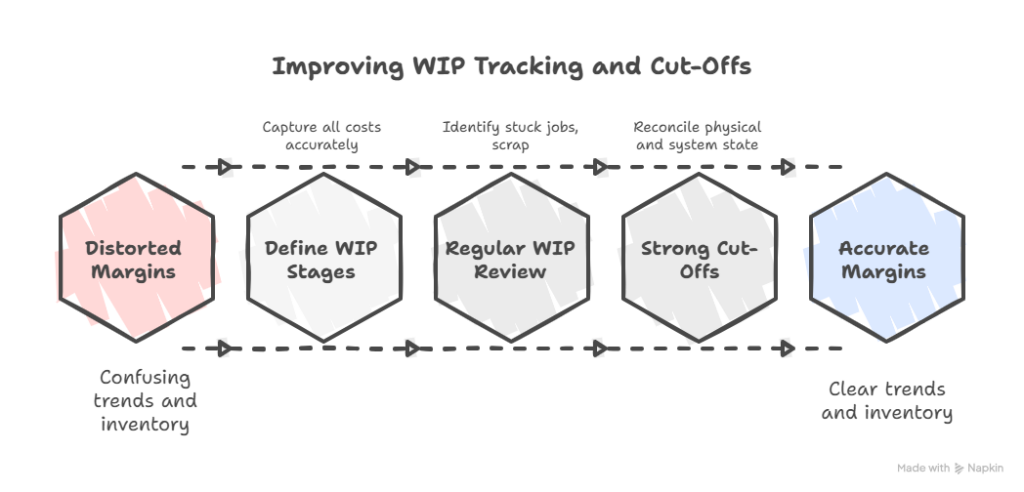

Weak WIP Tracking and Cut-Off Errors

Standard Costing vs Actual Costing Confusion

Many manufacturing plants use standard costing, but do not track actual variances properly, which leads to:

- Large, unexplained purchase price variances (PPV).

- Usage variances (materials consumed more than standard) not analysed.

- Overhead variances ignored, leading to wrong product profitability.

This makes management believe some products are profitable when they aren’t.

Resolution:

- Clear policy on whether the plant primarily uses standard cost or moving average/actual cost.

- Detailed variance analysis each month: material, labor, overhead, mix, yield.

- Feeding variance insights back into BOMs, routings, and purchasing strategy.

Excess and Obsolete Inventory Accumulation

- Scenario: A workwear manufacturer maintains 6 months of fabric inventory due to MOQ contracts.

- Outcome: Customer specification change renders ₹38 lakhs of stock obsolete.

- Result: Write-off of raw material + additional cost to procure new grade fabric.

- Lesson: Buffer stocks reduce risk, but without demand alignment, they destroy capital.

Inventory Shrinkage Due to Theft, Damage or Errors

To reduce shrinkage, manufacturers must implement:

- Serialized material identification

- Controlled access to storage

- Mandatory scrap reporting

- CCTV monitoring of warehouses

- Periodic cycle counts

Without controls, shrinkage silently drains profitability.

Cost Allocation Issues: Overhead, Labor, and Machine Time

Manufacturing costing isn’t just material it also includes:

- Direct labor (wages, overtime, incentives).

- Manufacturing overheads (power, maintenance, depreciation, factory rent).

- Machine hours or setup time for complex jobs.

When overheads are allocated using vague or outdated bases, high volume products may appear less profitable while low-volume, complex products look better than they truly are.

Resolution steps:

- Selecting rational overhead allocation bases (machine hours, labor hours, etc.)

- Periodic review of standard rates vs actual cost pool.

Using activity based costing (ABC) where complexity is high.

Compliance, Audit Readiness, and Management Reporting

Inventory is a key area in financial audits and internal control reviews. Common findings include:

- Weak documentation of standard costing assumptions.

- Inconsistent application of inventory valuation methods (FIFO, weighted average).

- Incomplete inventory disclosures for financial statements.

Without a strong inventory accounting framework, audits become time-consuming, and management gets delayed or unreliable MIS.

How structured processes help:

- Standardised inventory accounting policy and clear documentation.

- Tight linkage between inventory sub-ledgers and GL.

- Dashboards showing inventory days, ageing, variance trends, and margin impact.

How Kariwala & Co. LLP Supports US Manufacturing Companies

At Kariwala & Co. LLP, we work with US-based manufacturing businesses to:

- Diagnose inventory accounting pain points across raw materials, WIP, and finished goods.

- Clean up BOMs, WIP tracking, and standard costing so reported margins match operational reality.

- Design and run robust reconciliation routines between physical stock, production reports, and ERP ledgers.

- Build practical variance analysis and inventory dashboards that management can act upon.

We help finance leaders clarify and control inventory by merging US GAAP accounting knowledge with manufacturing operational insight.

Reference:

The Hidden Costs of Inventory Management — supply management trade article that explains how data inaccuracy, poor forecasting and outdated systems result in excess or obsolete stock and inefficiencies. ISM World